Real Estate

Real Estate Investing 201 - Doing The Analysis

When it comes to real estate investing, it’s very important to know whether this project is right for you, particularly if it’s profitable. As seasoned investors, we want to know every financial metrics about the investment opportunity, such as the NOI and the value-add opportunities. If you are new to real estate investing, you may be unfamiliar with breaking down the numbers and it’s perfectly normal when you’re just starting off. Here in this article, we talk about everything you need to know about the basics of analyzing a real estate deal.

Knowing The Terminology

When it comes to real estate investing, it’s very important to know the lingo that are commonly used. For those who are new to real estate investing or just want a quick revision on the terminology, we’ve got you covered. You can read it right here.

Residential Investment Opportunity Example

Earlier this week, your realtor found an interesting real estate investment property on the MLS. A legal duplex in the heart of downtown Toronto that was designed to be converted to a triplex or fourplex with a minor variance. Plumbing is already in place for that conversion. Currently, Unit A is on the main floor and is a two bedrooms/1 bathroom. On the upper floors, Unit B is a 2,000 square foot unit, that has 4 bedrooms/ 2.5 bathrooms. In addition, there is also an nanny suite being rented out. After a little bit of digging, your real estate investor sends you the following the document:

Listing Price

Legal Duplex and Nanny Suite – $1,000,000

Income

Unit A – $2,200 / month – utilities included = $38,400 / year

Unit B – $3,200 / month – utilities included = $22,800 / year

Nanny Suite – $800 / month – utilities included = $9,600 / year

Expense

Hydro – $500 / month = $6,000 / year

Gas – $400 / month – utilities included = $4,800 / year

Water & Water Heater rental – $150 / month = $1,800 / year

Taxes – $10,000 / year

Insurance – $5,000 / year

Snow Removal – $ 700 / year

1. Calculating Gross Operating Income

Although it is very helpful that your realtor had pulled together key information about the property, it is also important to verify the numbers yourself. With that said, lets get down into the analysis, starting with the potential gross income.

Potential rental Income = (Unit A Rent + Unit B Rent + Nanny Suite)

= $38,400 / year + $22,800 / year + $9,600 / year

= $70,800 / year

Since all of the units are rented out and are assumed to be paying the monthly rent on time, vacancy rate and credit loss is 0. As such, potential rental income is the same as effective rental income in this example. It is important to know your market’s vacancy rate and account for potential credit loss.

Effective Rental Income = Potential Rental Income – Credit Loss

= $70,800 / year – 0

= $70,800 / year

In our example, there are currently no other potential income generated by the rental property. As such, the gross operating income is the same as effective rental income. As an investor, you should look at how you can increase potential income generated by the rental property. Here are some common examples:

- On-premise coin-operated laundry machines

- On-premise vending machines

- Monthly parking permits

- Storage Unit fees

- Late Fees

Gross Operating Income = Effective Rental Income + Other Income Sources

= $70,800 / year + 0

= $70,800 / year

2. Calculating Operating Expenses

In this example, we were given various expenses related to the rental property. Operating expense can depend on the property and how it is managed. Some operating expenses can include:

- utilities – gas, heat, hydro and water

- insurance

- taxes

- maintenance and repairs

- property management fees – marketing, advertisement, accounting and legal work

- other services – gardening, garbage and snow removal

As such, the operating expense for our example is the following.

Operating Expense = (Hydro + Gas + Water + Taxes +Insurance and Snow Removal)

= $6,000 / year + $4,800 / year + $1,800 / year + $10,000 / year + $5,000 / year + $ 700 / year

= $28,300 / year

As a successful real estate investor, it’s not only important to increase your gross operating income, but to also decrease operating expenses in order to maximize your property’s true potential value. For example, your tenants could be responsible for covering utilities.

3. Calculating Profitability

Using the information above, we can calculate the Net Operating Income (NOI) and determine how profitable it is to invest into this project.

NOI = Gross Operating Income – Operating Expenses

= $70,800 / year – $28,300 / year

= $42,500 / year

Even though the project is profitable, you are likely not going to purchase this real estate investment with 100% cash but rather leverage other people’s money to do so. As real estate investors, it’s important to explore all sources of alternative financing, such as a mortgage from a bank or financial institution. Assuming a 20% down payment and a 800k mortgage at a 2% interest rate with a 30-years amortization period, the monthly payment is $2,954 and annual debt service is $35,484. Given the following information, you can determine how much this real estate investment cash flows and how much money you are putting into our pockets for being a landlord.

Cash Flow = Net Operating Income – Annual Debt service

= $42,500 / year – $35,484 / year

= $7,016 / year ($584.67 / month)

Real estate investors often use capitalization rate to estimate the investor’s potential return on their investment and how it compares with other real estate investments in their local market. It is important to understand your local market’s capitalization rate, based on the real estate property type and building class. Similar to other financial metrics for profitability, the higher the capitalization rate is, the better the investment.

Capitalization Rate = Net Operating Income / Current Value of the Property

= $42,500 / year / $1,000,000

= 4.25%

Real estate investors also use return on equity (ROE) to determine the return on an investment relative to the real estate investor’s equity in that investment. Similar to other financial metrics for profitability, the higher the ROE is, the better the investment. Assuming a 20% down payment and a 800k mortgage at a 2% interest rate with a 30-years amortization period, the monthly payment is $2,954 and annual debt service is $35,484. After 1 year of successfully running the real estate property, the real estate property value increased by 3%. Given the following information, you can determine the ROE and how efficient the investment is and how it compares to other investment opportunities, such as other businesses, real estate and stocks.

ROE = Net Income / Investor’s Equity

= ($42,500 + 0.03*$1,000,000) / ($200,000 + $35,484)

= 30.08%

Remember, net income is the sum of all the net operating income over a period of time and appreciation in property value. Investor’s equity can be a bit tricky. Investor’s equity is how much cash is personally “tied up” with the investment property. Initially, the investor’s equity is just the down payment, closing costs as well as any immediate maintenance and repairs. In our example, we assumed that the building required no closing costs, maintenance and repairs. It is important to note that investor’s equity changes with time. Over time, the investor’s equity will increase as more money becomes “tied up” to the property. For example, there are mortgage payments, carrying costs, maintenance and repairs. If you want the full list of other additional expenditures that can affect ROE, you can find that in the consideration section below.

4. Calculating Debt

If you’re borrowing a large sum of money, lenders are interested in knowing how high-risked/leveraged the investor is. As such, lenders may use the loan-to-value (LTV) ratio or leverage ratio:

Leverage Ratio = Total Debt / Total Equity

= $800,000 / $200,000

= 4

LTV Ratio = Total Debt / Current Value of the Property

= $800,000 / $1,000,000

= 0.8

In this example, the leverage and LTV ratio were 4 and 0.8 respectively. Generally, most lenders offer mortgage and home-equity applicants the lowest possible interest rate when the LTV ratio is at or below 0.8 and leverage ratio is at or 4. When the LTV is above 0.8, the individual is considered a higher risk and lenders may charge a higher interest rate as such. In addition, higher-risked individuals may also need to purchase mortgage loan insurance as this protects your lender in case you can’t make your payments. Lenders are also interest in knowing an investors ability to pay back their debt obligations. As such, they would use the debt service coverage (DSC) ratio.

DSC Ratio = Net Operating Income / Annual Debt Service

= $42,500 / year / $35,484 / year

= 1.20

For this example, the DSC ratio is about 1.20. In general, lenders want to protect themselves by having a certain level of safety margin when lending money to real estate investors. Lenders often require a DSC ratio of 1.2 or higher when considering loan applications for rental property and other real estate ventures. If the economy is growing, lenders may be more forgiving and lower the required lower DSC ratio.

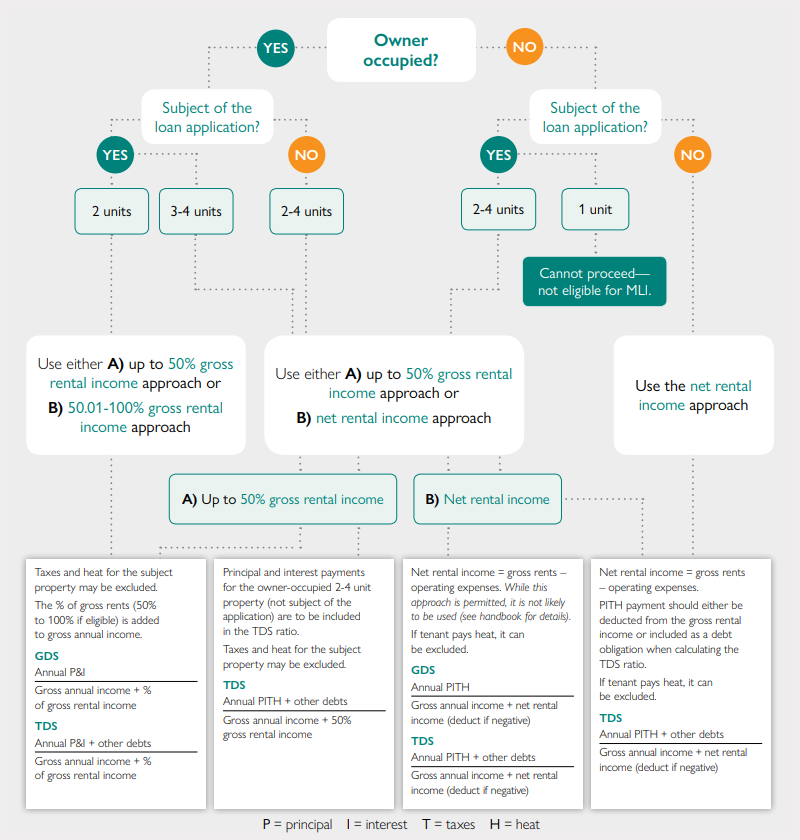

When it comes to underwriting a mortgage, financial institutions will also look at an investor’s debt ratios to decide lending eligibility. There are two ways for lenders to calculate your debt ratios: gross debt service (GDS) ratio or total debt service (TDS) ratio. If you would like to learn more information about TDS and GDS ratio, you can find that here. In order to evaluates the borrower’s risk and their ability to repay the mortgage, lenders determine that your debt (car payments, student loans, credit card bills, etc.) does not exceed a certain percentage of your income. In general, financial institutions use a GDS of 35% and TDS of 42% as maximum limits. When it comes to rental properties, TDS and GDS ratios will account for rental income into its calculation. Unlike residential property for personal use, GDS and TDS calculations can vary and depend on the certain factors. For example, is the rental property owner occupied, is the rental property subject of the current loan application, and the number of units in the property. Below, is a flow chart, provided from CMHC, to help you identify how financial institutions calculate your GDS and TDS. You can more information about it here.

Considerations

1. Location

It is very important to consider the property’s location, such as its proximity to amenities and the neighborhood’s status. As real estate investors, it’s important to consider the property’s location and how the area is expected to evolve over the investment period. For example, the empty land at the back of a residential building could someday become a noisy manufacturing facility and thus, diminishes the property’s value.

2. Value-Add Opportunities

Value-add opportunities are methods to increase a real estate investment’s cash flow over time by making improvements to the property. In this example, the real estate property is currently a duplex but has the potential to be converted into a triplex or fourplex. If executed properly, it can increase the net operating income at the property and can result in the property appreciating in value. It is important to note that there are also increased risks in doing so. Not only does the investor requires additional financing for the improvements, but there is also municipal/provincial by-laws that the investor will have to successfully jump through, prior to recouping the original investment.

3. Additional Expenditures

We know there are various expenses related to running a rental property, such as the operating costs associated to being a landlord. It is also important to consider variable costs into your analysis. These can arise prior to, during or after your real estate purchase. Some of the additional expenditures can include:

- Inspection – general home inspection, electrical inspection, septic inspection and well inspection/water inspection.

- Environmental site assessment – real estate properties that have environmental contaminants may require phase I, II and/or III assessments.

- Legal Fees – title insurance, title search costs, title registration costs.

- Mortgage fees – lender fees and/or penalty on current mortgage.

- Land transfer taxes – see here for more details.

- Carrying costs during renovation, maintenance and repairs – mortgage payments, property taxes and utilities.

- renovation, maintenance and repairs – current and deferred.

Need help finding an Investment Property In the GTA?

We Are Available 24/7

Feel free to ask us anything.

We are fluent in 廣東話 Cantonese and English

Social Media

Interested In Learning More?

Real Estate Chattels and Fixtures – What’s Included and What’s Not Sometimes, life throws you a curve ball. Imagine yourself finally getting …

Real Estate Home Improvements – Inexpensive Projects You Can Try For Big Returns It’s always a good idea to spruce up the …

Real Estate Property Easements – Enjoying Your Property To Its Fullest When it comes to real estate, what you don’t know CAN …

Our Promise To You

Fung Finances is a free service. We are not an accountant, financial advisor, law firm, “lawyer referral service,” or a substitute for an accountant, financial advisor, attorney, or law firm. Always do your own due diligence and never blindly listen to a random article on the internet. We do our best to provide financial education with our free videos, articles, tools, and other self-help content. But these are for informational purposes only, they’re not investment advice.

Fung Finances does not and cannot guarantee the accuracy or applicability of any information regarding your individual circumstances. The examples we provide are hypothetical and we encourage you to get advice from a qualified professional regarding specific investment, tax, legal, and financial issues. Previous market performance does not guarantee future performance.

We want everyone to be able to make educated financial decisions. We do not feature every company or financial product available. However, we’re proud of the financial education and guidance that we provide at no charge.

We’re paid by our brand partners and advertisers. This may influence which products we mention, review, and where they appear on our site. But it does not affect our recommendations or advice.